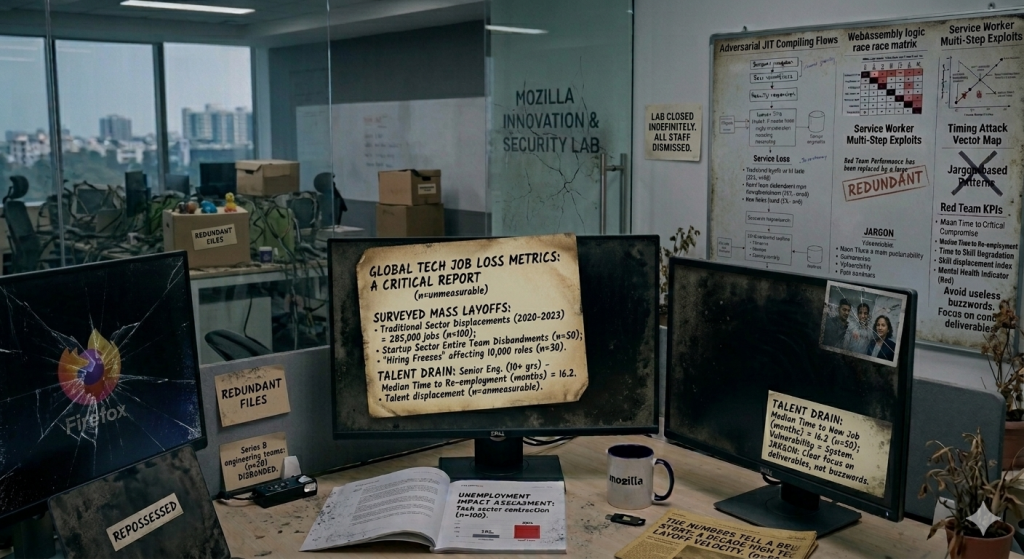

The Numbers Tell a Brutal Story

I’ve been covering tech for over a decade, and I’ve never seen anything quite like this. The data coming out of major tech hubs shows unemployment rates that dwarf both the 2008 financial crisis and the early pandemic chaos of 2020. We’re talking about a fundamental shift, not just a temporary correction.

What’s particularly striking is how this isn’t limited to any single segment. Sure, we’ve seen the headline-grabbing mass layoffs at Meta, Amazon, and Google. But the real story is in the smaller companies—the Series B startups quietly letting go of entire engineering teams, the mid-stage companies freezing all hiring indefinitely.

The ripple effects are everywhere. I’m hearing from senior engineers with stellar resumes who’ve been job hunting for six months or more. These aren’t fresh graduates struggling to break in; these are people with 10+ years of experience at companies you’d recognize, suddenly finding themselves competing for entry-level positions.

Here’s what’s really unsettling: the velocity of this downturn. The 2008 crisis took months to fully manifest in tech. The pandemic initially created a hiring boom before the correction. This time, the floor just dropped out seemingly overnight.

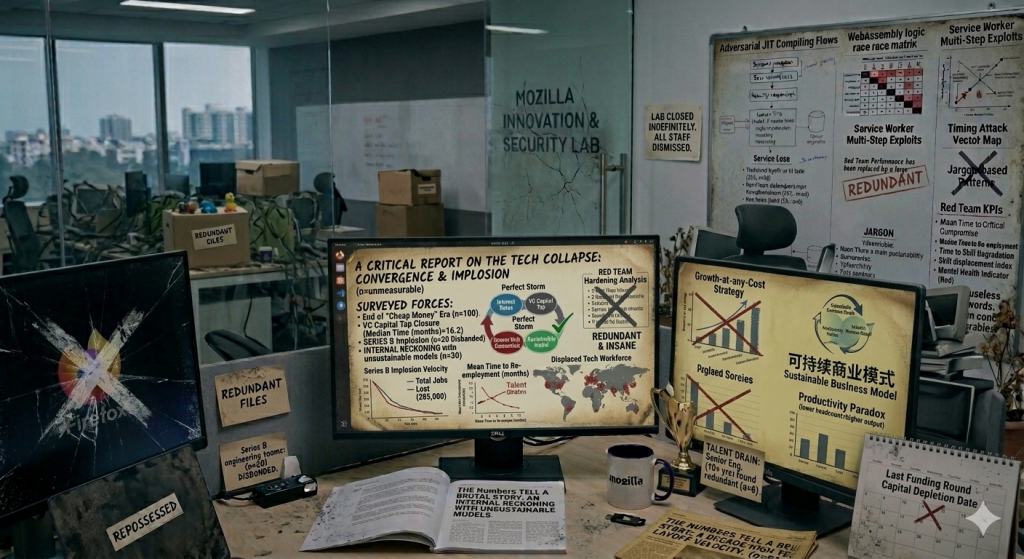

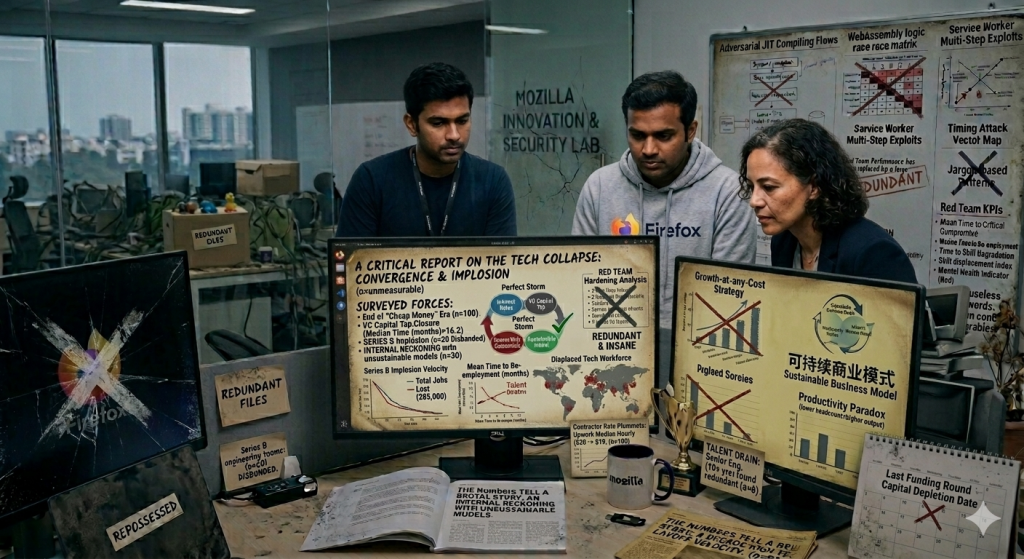

The Perfect Storm Behind the Collapse

This isn’t just about interest rates, though that’s certainly part of it. We’re seeing the convergence of multiple forces that have fundamentally altered how tech companies operate. The cheap money era is over, and suddenly all those growth-at-any-cost strategies look absolutely insane.

I think what’s caught everyone off guard is how quickly the venture capital tap turned off. LPs got spooked, and now even promising startups are struggling to raise bridge rounds. Without that constant influx of capital, companies that were burning through millions monthly suddenly had to face reality.

The other factor that’s not getting enough attention is the productivity paradox. Companies realized during the layoffs that they could maintain—or even improve—output with significantly fewer people. That’s a sobering wake-up call about how bloated many tech teams had become during the boom years.

What’s interesting here is how this differs from previous downturns. In 2008, the problem was external—financial markets collapsed. In 2020, it was a black swan event. This time, it feels more like an internal reckoning with unsustainable business models that were propped up by artificially cheap capital for way too long.

Who’s Getting Hit Hardest

The casualties aren’t distributed evenly, and that’s telling us a lot about where the industry is heading. Mid-level engineers and product managers seem to be bearing the brunt of this downturn. Companies are keeping their absolute top performers and their junior talent—who are cheaper—while gutting the middle layers.

Geographic disparities are stark too. Seattle and San Francisco are bloodbaths, but I’m seeing surprising resilience in places like Austin and Denver. Remote work has democratized talent, but it’s also democratized the pain when companies decide to cut costs.

Here’s the thing that’s really bothering me: diversity and inclusion programs are getting decimated. All that progress we made over the past decade is evaporating as companies retreat to their comfort zones during hiring freezes. It’s frustrating to watch, but unfortunately predictable.

The contractor and gig economy side is even worse. Companies are cutting external consultants first, and platforms like Upwork are seeing rates plummet as desperate tech workers flood the freelance market. It’s creating a race to the bottom that’s hurting everyone.

What This Means for Tech’s Future

I’ve been thinking a lot about what comes next, and honestly, I don’t think we’re going back to the way things were. This feels like a permanent reset in how tech companies approach hiring and growth. The days of throwing engineers at problems without clear ROI metrics are probably over for good.

There’s going to be a flight to quality that benefits the strongest companies and the most talented individuals. Google, Microsoft, and Apple will eventually emerge from this stronger, having picked up top talent at bargain rates. Meanwhile, weaker players are going to struggle to compete when capital becomes available again.

What’s particularly interesting is how this might accelerate consolidation. Startups that might have competed with incumbents will instead get acquired for talent and IP at fire-sale prices. We’re already seeing early signs of this, and I expect it to accelerate through 2024.

The silver lining—if you can call it that—is that this correction might force the industry to focus on sustainable business models again. Maybe we’ll see fewer companies burning billions on customer acquisition and more emphasis on actually building profitable businesses. That wouldn’t be the worst outcome from all this chaos.

The tech industry is experiencing its most severe employment crisis in recent memory, and the old playbooks don’t apply here. This isn’t a temporary blip—it’s a fundamental restructuring that will reshape how we think about tech careers, company building, and growth strategies. The companies and individuals who adapt to this new reality will thrive, but it’s going to be a painful transition for everyone else.